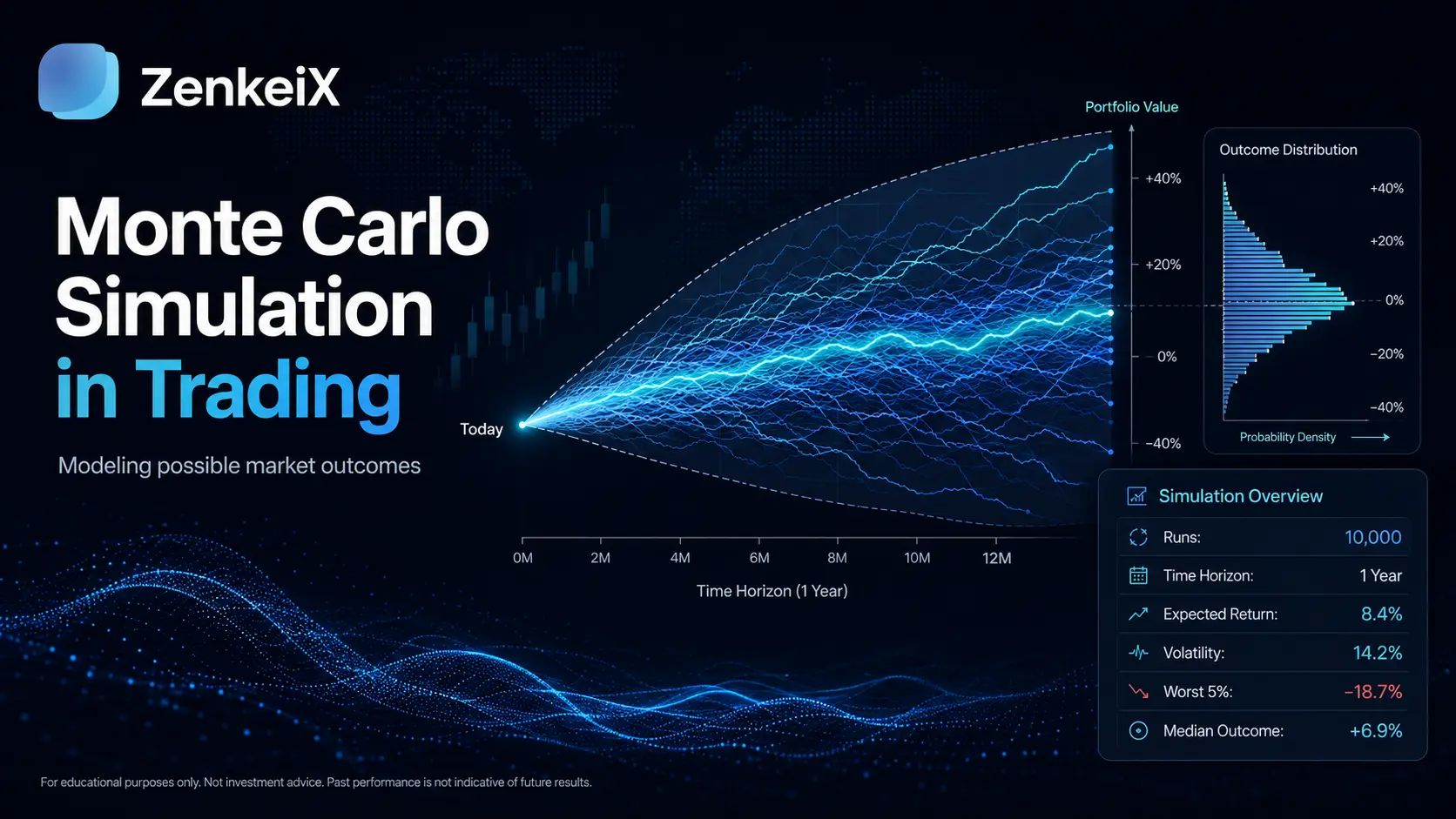

What Monte Carlo simulation in trading is

Monte Carlo simulation in trading is a method for testing a strategy across many possible scenarios instead of trusting a single historical path. It takes trades, returns, or operating assumptions and recombines them into hundreds or thousands of alternative equity paths.

The goal is not to predict the future. The goal is to see how fragile the strategy can become when the future does not copy the backtest.

Why a beautiful backtest is not enough

A backtest can be elegant, rising, and convincing. But it often tells one sequence only: that exact order of trades, that volatility, that market regime, that combination of entries and exits.

The problem is that live trading does not give you trades in the most comfortable order. Losses can arrive before profits. Drawdown can concentrate when size is higher. The strategy can keep the same edge but follow a path that is psychologically and financially much harder.

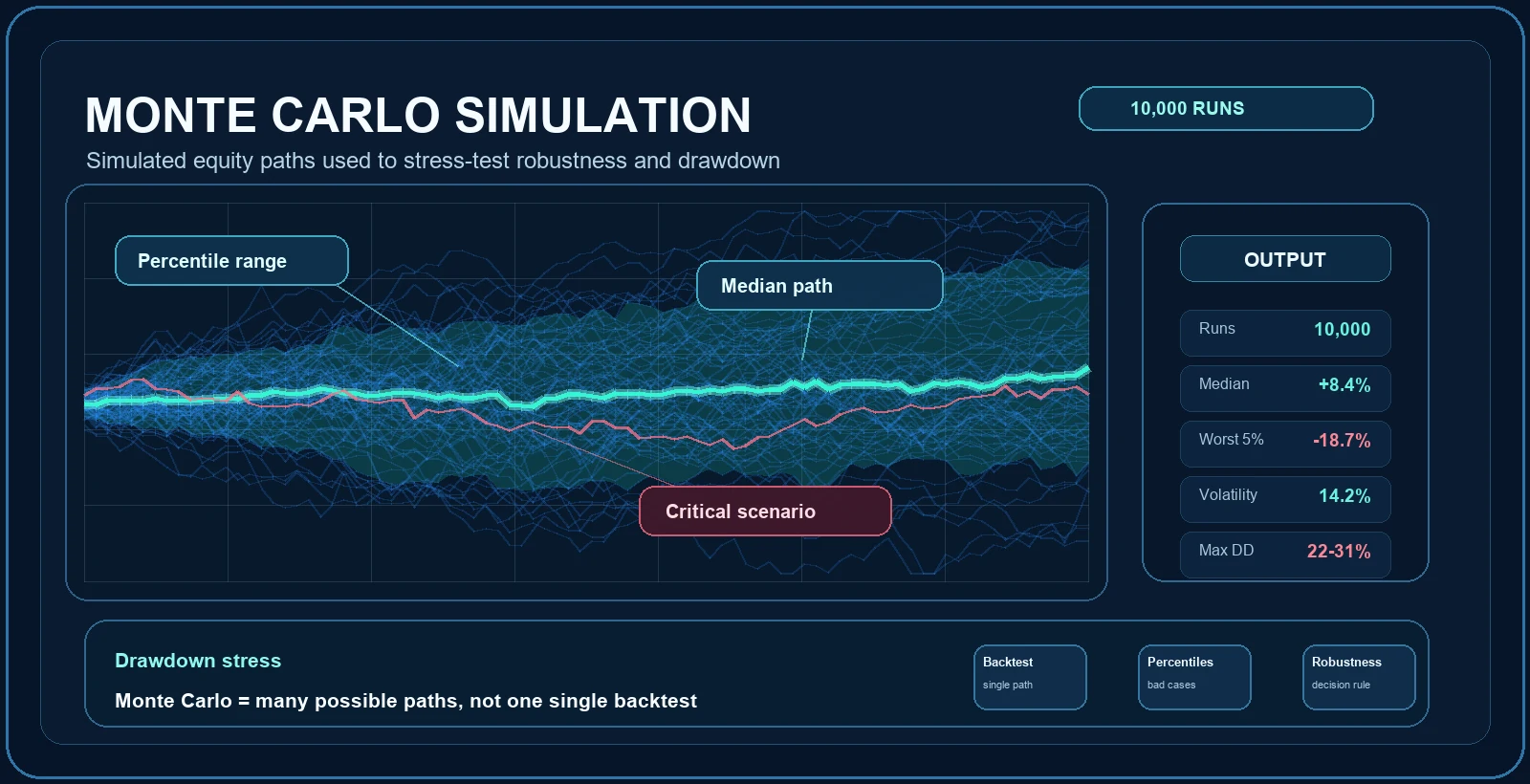

This is why Monte Carlo connects directly with metrics such as maximum drawdown, Value at Risk, and Ulcer Index. It is not enough to know how much a strategy made. You need to know how badly it could have hurt.

How Monte Carlo works on a trading strategy

In trading, Monte Carlo simulation can be built in several ways. The simplest approach reshuffles the order of historical trades. More advanced versions resample returns, add slippage, change volatility, or simulate execution errors.

- trade shuffle: changes the order of historical results

- return bootstrap: resamples individual returns or blocks of returns

- cost and slippage stress: worsens realistic execution conditions

- parameter variation: checks whether the system remains stable near selected settings

- risk of ruin simulation: measures the probability of unsustainable drawdown

For an Expert Advisor, this check is essential: a system should not look good only in a report. It should stay credible when event sequence changes.

What to read in Monte Carlo results

The important part is not generating a thousand colorful curves. The important part is understanding what they say. If simulations diverge too much, the backtest is fragile. If the worst case is unbearable, sizing is too aggressive. If percentile drawdown is much worse than historical drawdown, the original report was too comfortable.

- median drawdown and 90th or 95th percentile drawdown

- final capital range after N trades

- probability of ending below a defined threshold

- maximum losing streak

- risk of ruin or probability of crossing a drawdown limit

This is where Recovery Factor, K-Ratio, and Sortino Ratio become useful: Monte Carlo stresses the path, the metrics read risk quality.

Common mistakes when using Monte Carlo

The biggest mistake is treating Monte Carlo as decoration for the backtest. If it is only there to add another chart, it does not help. It should become a decision rule.

- ignoring worse costs, spread, and slippage

- trusting too few historical trades

- ignoring dependence between trades and market regimes

- looking only at the average curve instead of bad percentiles

- not reducing size when the critical scenario is too hard

A good system is not the one that produces the prettiest curve. It is the one that still makes sense when the path gets messy.

Want to understand whether your Expert Advisor is robust or just well optimized?

We can analyze backtest, Monte Carlo, drawdown distribution, sizing, and parameter stability to understand whether the system can handle real conditions.

FAQ

Does Monte Carlo predict the future?

No. It stresses the strategy across many possible paths. It does not predict which path will actually happen.

How many trades are needed for a useful simulation?

The more trades you have, the more informative the test becomes. With very few trades, Monte Carlo may reveal fragility, but it cannot make the sample magically reliable.

Is it useful for Expert Advisors?

Yes. It is one of the most useful checks for understanding whether an EA depends too much on a lucky trade sequence or over-optimized settings.

Does Monte Carlo replace forward testing?

No. It complements it. Monte Carlo stresses the backtest, while forward testing checks behavior on new data.